FIRST QUARTER 2026 INTERIM MANAGEMENT STATEMENT

Strong first quarter performance with continued revenue momentum

Full year adjusted EPS expected at the upper end of the guidance range

29 April 2026 – Glanbia plc, the Better Nutrition company (“Glanbia” or the “Group”), is issuing this Interim Management Statement for the three month period ended 4 April 2026 (“the period”, or “Q1 2026”). This statement is issued in conjunction with the Group’s Annual General Meeting (“AGM”) which is being held today.

Q1 2026 Highlights 1 :

- Group like-for-like (“LFL”) revenue growth of 7.2% with strong volume growth across all three segments;

- Performance Nutrition (“PN”) LFL revenue growth of 11.5%;

- Optimum Nutrition LFL revenue growth of 18.8% with accelerating category growth, new distribution and continued innovation;

- Health & Nutrition (“H&N”) LFL revenue growth of 11.6%;

- Volume growth of 12.5% driven by strong demand across priority end-use markets;

- Dairy Nutrition (“DN”) LFL revenue growth of 2.0% with strong volume and pricing growth in protein solutions;

- Progress on Group-wide transformation programme, targeting annual savings of at least $60m by 2027;

- €22.2 million returned to shareholders via share buybacks year-to-date; and

- FY 2026 adjusted EPS expected to be at the upper end of medium-term guidance of 7% to 11% constant currency.

Commenting today Hugh McGuire, Chief Executive Officer, said:

“I am pleased to report that Glanbia delivered a strong performance in the first quarter, with Group like-for-like revenue growth of 7.2% across our portfolio of better nutrition brands and ingredients with volume growth in all three segments, benefitting from accelerating category growth and good end-use market demand.

Performance Nutrition showed continued momentum, with like-for-like revenue growth of 11.5%, led by our Optimum Nutrition brand with volume and pricing growth. Health & Nutrition delivered double-digit volume growth driven by continued demand in its priority end-use markets. Dairy Nutrition saw strong volume and pricing growth in protein solutions.

We continue to see strong demand for our brands and ingredients and remain focused on executing on our medium-term strategy, notwithstanding the current geopolitical uncertainty. As a result of the Group’s performance in Q1, we now expect adjusted EPS growth in FY 2026 to be at the upper end of the medium-term guidance range of 7% to 11% constant currency.”

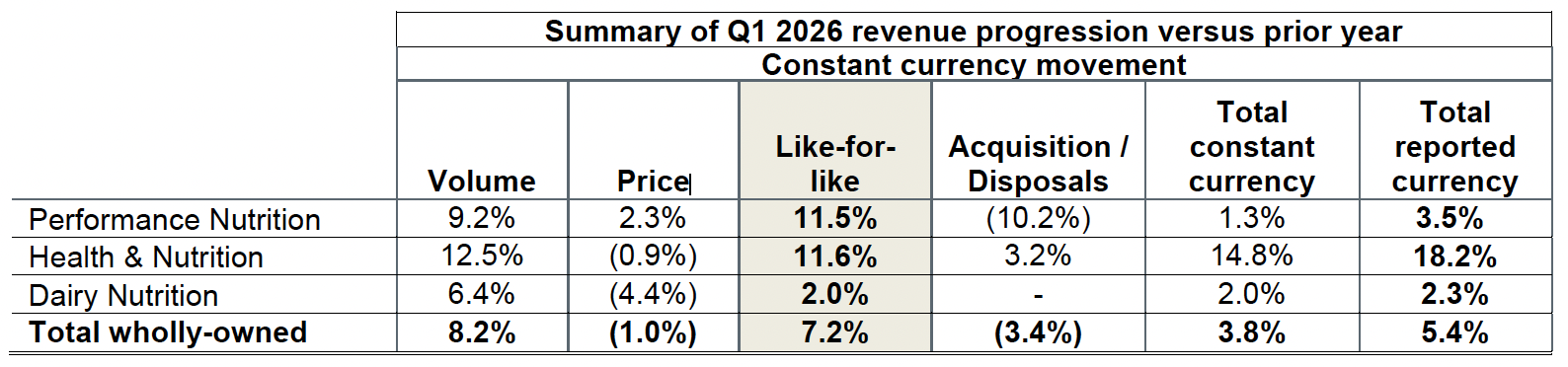

Summary revenue progression (all commentary is on a constant currency basis)

In the three months ended 4 April 2026, Group LFL revenue increased by 7.2% compared to the same period in 2025, driven by a volume increase of 8.2%, slightly offset by a price decrease of 1.0%. Total Group revenue increased by 3.8% as a result of LFL revenue growth of 7.2%, partly offset by a decrease of 3.4% from the net impact of acquisitions and disposals.

Performance Nutrition

PN LFL revenue increased by 11.5%, with a volume increase of 9.2% and a price increase of 2.3%. Volume growth was driven by continued strong category growth, new distribution, lapping of a weaker comparative and innovation. Pricing growth was as a result of price increases implemented in the Americas in Q4 last year, somewhat offset by promotional activity and tactical price reductions on products in the energy category.

PN Americas, which represented 57% of PN revenue, saw LFL revenue increase by 4.0%, with volume growth in Optimum Nutrition and Isopure somewhat offset by declines in other portfolio brands. PN International, which represented 43% of PN revenue, saw LFL revenue increase by 23.4%, driven by strong volume and pricing growth across international markets, with momentum for Optimum Nutrition evident across priority regions.

Optimum Nutrition, which represented 78% of PN revenue, delivered an 18.8% increase in LFL revenue during the quarter and US consumption2 growth of 13.3% in the last 13 weeks.

Health & Nutrition

Health & Nutrition is a better nutrition global solutions partner, combining insight, science and high-quality ingredients to help customers create great-tasting products for healthier lives. H&N focuses on attractive, high-growth end-use markets including Active Nutrition, Functional Beverages and Vitamins, Minerals & Supplements. H&N revenue increased by 11.6%, driven by a 12.5% increase in volume, a 0.9% decrease in price and a 3.2% increase from the impact of the acquisitions of Sweetmix and Scicore. We continue to make good progress on capacity expansions in H&N in the US, China and Europe. Volume growth was driven by a strong performance in EMEA and ASPAC with continued momentum in key end-use markets. The price decline was due to pass through pricing with customers.

Dairy Nutrition

Dairy Nutrition is a leading producer of whey proteins and American-style cheddar cheese in the US and provides a wide range of functional protein solutions and bioactives. DN revenue increased by 2.0%, with a 6.4% increase in volume, somewhat offset by a 4.4% decrease in price. The increase in volume was driven by strong end-use markets with demand for high end whey proteins growing strongly with double-digit volumes in protein solutions. The decrease in price was a result of negative cheese markets in the first quarter of the year, somewhat offset by double-digit pricing in whey protein solutions.

Share buyback

Between 25 February 2026 and 27 April 2026, Glanbia returned €22.2 million to shareholders via its share buyback programme, repurchasing and cancelling 1,296,487 ordinary shares on Euronext Dublin at an average price of €17.14.

Financing

The Group’s balance sheet remains in a strong position. Glanbia's net debt as at 4 April 2026 was $648 million, an increase of $69 million versus the net debt position at the end of Q1 2025. At the end of the period the Group had committed debt facilities of $1.4 billion.

2026 Outlook

Glanbia saw strong momentum in the first quarter across all three segments, and while the Group continues to closely monitor the ongoing geopolitical environment, based on current expectations for the remainder of the year, the Group now expects FY 2026 adjusted EPS growth to be at the upper end of its medium-term guidance of 7% to 11% constant currency. PN and H&N revenues are now expected to be at the upper end of their medium-term guidance ranges and DN EBITDA is now expected to be in the range of $160 million to $170 million. All other guidance is aligned to our medium-term outlook.

Annual General Meeting

Glanbia is hosting its AGM at 11.00 a.m. (BST) today at the Killashee Hotel, Naas, Co. Kildare, Ireland.

Ends

1 Like-for-like revenue growth excludes the net impact from acquisitions and disposals and is shown on a constant currency basis.

2 Consumption growth is US measured channels and includes online, FDMC (Food, Drug, Mass, Club) and specialty channels. Data compiled from published external sources and Glanbia estimates for the 13 week period to 4 April 2026.